Energy Prices and Geopolitical Tensions

Stubborn inflation has been linked in part to higher energy costs. Crude benchmarks have climbed during an 11-week conflict involving Iran, increasing transportation and production expenses across sectors. The surge has filtered into consumer prices and complicated the central bank’s efforts to steer inflation back to its target range.

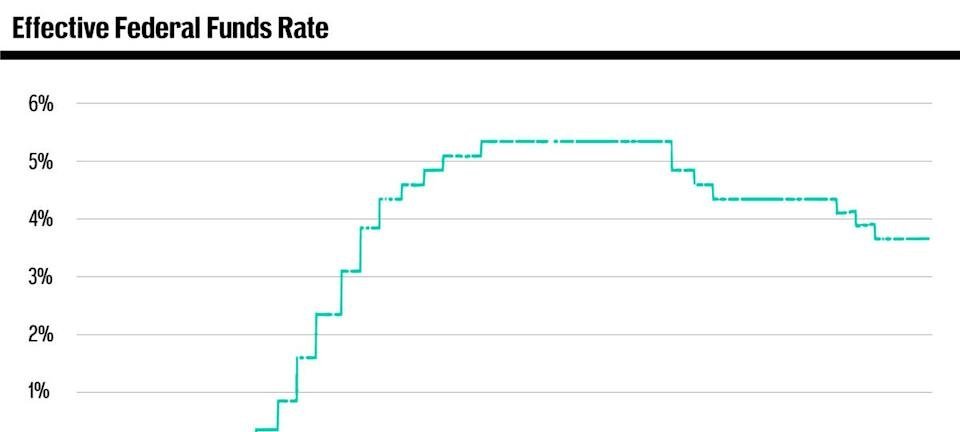

At its 29 April policy meeting, the Federal Open Market Committee voted 8-to-4 to keep the benchmark federal funds rate unchanged at 3.50% to 3.75%. According to the Fed’s meeting records, that split represented the narrowest margin of agreement among policymakers since 1992, reflecting diverging views on how long rates should remain elevated. Under the Fed’s dual mandate, officials must balance maximum employment against stable prices, a task made more difficult when labor demand stays firm even as inflation lingers.

Market Expectations Recalibrated

Investor sentiment has adjusted swiftly. The CME FedWatch Tool shows futures traders assigning the highest probability to the next rate cut occurring in mid-to-late 2027, mirroring Bank of America’s updated call. Some market participants are even bracing for the possibility that rates could rise again before they decline. The Kalshi prediction market currently places the odds of a hike before July 2027 at 47%, highlighting uncertainty around the trajectory of policy.

Bond markets have echoed that caution. Yields on two-year Treasury notes, which are sensitive to monetary policy expectations, have edged higher as traders price in a longer period of restrictive settings. Analysts say the stance reflects concern that inflation could re-accelerate if energy prices climb further or supply chain strains intensify.

Key Inflation Reports Ahead

The Bureau of Labor Statistics is scheduled to release the April Consumer Price Index on 12 May. Economists surveyed ahead of the report estimate headline CPI rose 0.6% month over month and 3.7% from a year earlier. Core CPI, which excludes food and energy, is expected to increase 0.3% on the month and 2.7% on the year. By comparison, the March headline rate stood at 3.3% annually.

Imagem: Internet

Another closely watched gauge, the Personal Consumption Expenditures Price Index, accelerated in March, according to data published by the Bureau of Economic Analysis on 30 April. The headline PCE advance was largely attributed to rising energy costs, reinforcing concern that external shocks may continue to feed through to broader price levels.

Implications of a Prolonged Hold

Extended high interest rates influence multiple corners of the economy. Elevated borrowing costs can discourage corporate investment, dampen consumer spending on big-ticket items and ease upward pressure on wages. At the same time, leaving rates restrictive may bolster real yields, attracting foreign capital and supporting the U.S. dollar, which in turn can weigh on export competitiveness.

Monetary policy remains one part of a larger policy framework directed at inflation containment. Fiscal outlays, supply chain adjustments and geopolitical developments are also shaping the price outlook. The International Monetary Fund, in its most recent World Economic Outlook, cautioned that energy shocks and labor shortages could complicate central banks’ efforts to restore price stability worldwide.

How the Outlook Could Change

The path of rates will hinge on forthcoming data. Should monthly inflation figures moderate convincingly and wage growth slow, policymakers could regain confidence that underlying price pressures are easing. Conversely, further upside surprises could reinforce the case for maintaining—or even raising—current rates.

For now, Bank of America’s new timeline places it among the more hawkish forecasts in the analyst community, though not an outlier. The divergence of views across brokerages highlights the difficulty of projecting policy in an environment of mixed signals: strong payrolls, sticky services inflation and heightened geopolitical risk.

As the Federal Reserve navigates these cross-currents, officials have signaled they will continue to base decisions on incoming information rather than preset schedules. With markets now anticipating that any relief will arrive no sooner than 2027, attention will focus on each inflation release, employment report and policy speech for clues to whether that horizon might shift again.