Parent PLUS loan transition window

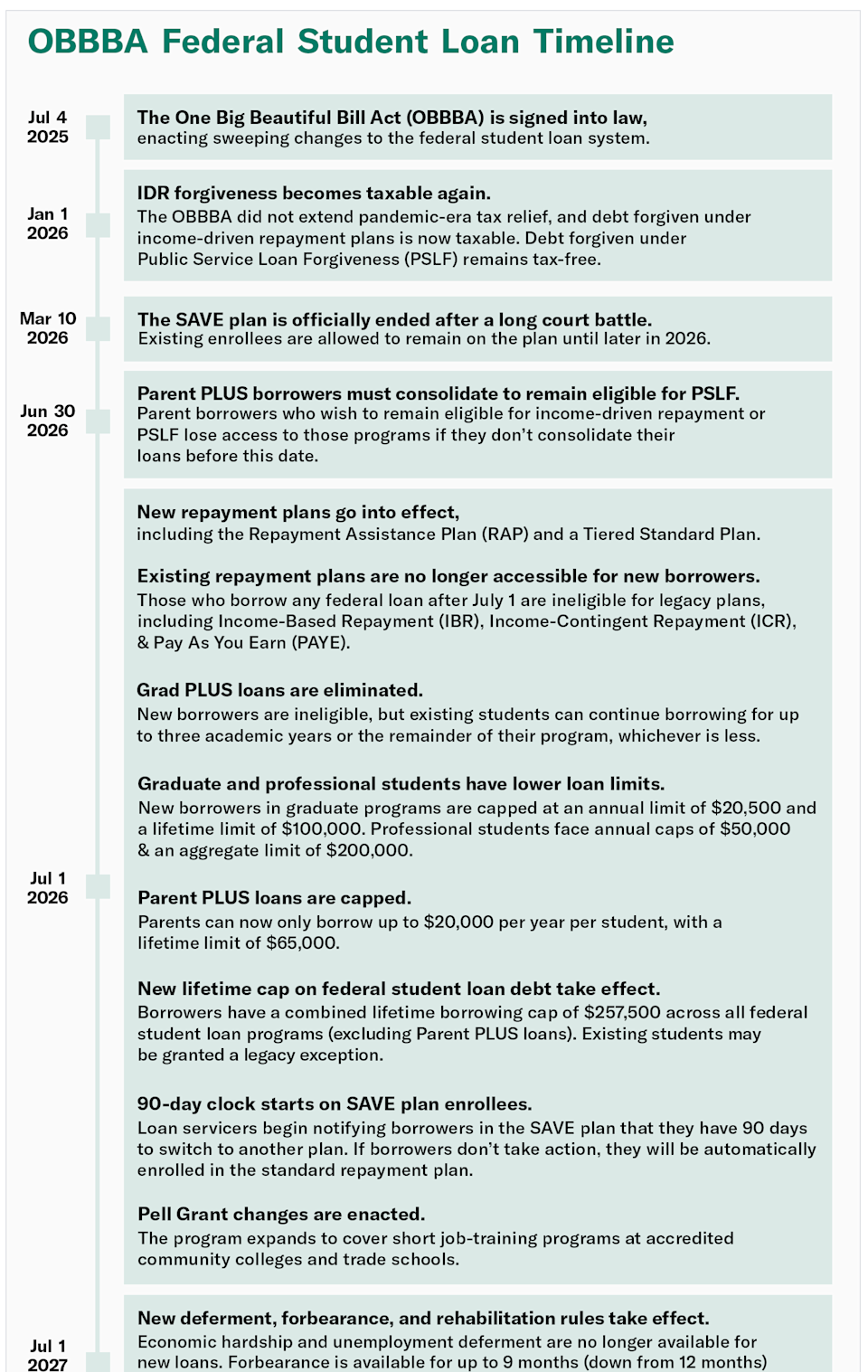

Families financing education through the Parent PLUS program also face looming changes. The statute closes a grandfathering option that currently allows parents to convert PLUS balances into federal consolidation loans and then enter income-driven repayment. Under the new rules, that path disappears after June 30, 2026. Financial-aid offices have begun alerting borrowers that missing the deadline could lock them into higher standard payments.

Pell Grant adjustments

On July 1, 2026, colleges will calculate Pell Grant awards with a schedule tied to the federal poverty line rather than the Expected Family Contribution formula. While the act does not alter the maximum award amount for the 2026–27 year, it redefines student eligibility, particularly for independent enrollees. Prospective recipients are being advised to review household income documentation ahead of the Free Application for Federal Student Aid (FAFSA) cycle that opens in October 2025.

End of tax-free forgiveness

An earlier provision of pandemic-era relief made most discharged student debt exempt from federal income tax through December 31, 2025. That exemption expires before the OB BBA implementation date, meaning balances forgiven under any program after January 1, 2026, will generally be treated as taxable income under current Internal Revenue Service guidance. Borrowers pursuing loan-forgiveness pathways are encouraged to consult authoritative resources, such as the U.S. Department of Education’s Federal Student Aid website, for updated tax implications.

Creation of the Repayment Assistance Plan (RAP)

The RAP becomes the primary income-driven option when the SAVE plan closes. Under RAP, monthly obligations will be calculated as a percentage of discretionary earnings, with forgiveness triggered after a fixed number of qualifying payments. Detailed thresholds and percentage rates will appear in forthcoming regulations that the Department of Education is required to publish no later than April 1, 2026.

Imagem: Internet

Current enrollees in legacy income-driven plans may transition to RAP automatically, remain in their existing plan if permitted, or select a different fixed-payment schedule. The law directs loan servicers to provide at least two written notices outlining available choices before any automatic migration occurs.

Potential elimination of additional plans

The OB BBA authorizes the Secretary of Education to streamline the repayment portfolio by closing plans deemed redundant. While the statute does not specify which programs could disappear, policy analysts have flagged Pay As You Earn (PAYE) and Income-Based Repayment (IBR) for review. A final decision is expected after a negotiated-rulemaking process slated for late 2026.

Outlook for 2027 and 2028

Beyond the initial rollout, the act schedules periodic reviews of borrowing limits, with the next assessment due by July 1, 2027. Any resulting adjustments would apply to loans first disbursed on or after that date. Additionally, the Government Accountability Office must deliver a report to Congress by March 1, 2028, evaluating RAP’s cost to taxpayers and its effect on delinquency rates. Lawmakers could use those findings to propose further amendments.

Until those future benchmarks arrive, students, parents, and graduates face a compressed timeline to evaluate existing debt, anticipate tax liabilities, and choose repayment strategies compatible with the new regulatory framework. Financial-aid officers and loan servicers are expected to release step-by-step transition guidance as the July 1, 2026, effective date approaches.