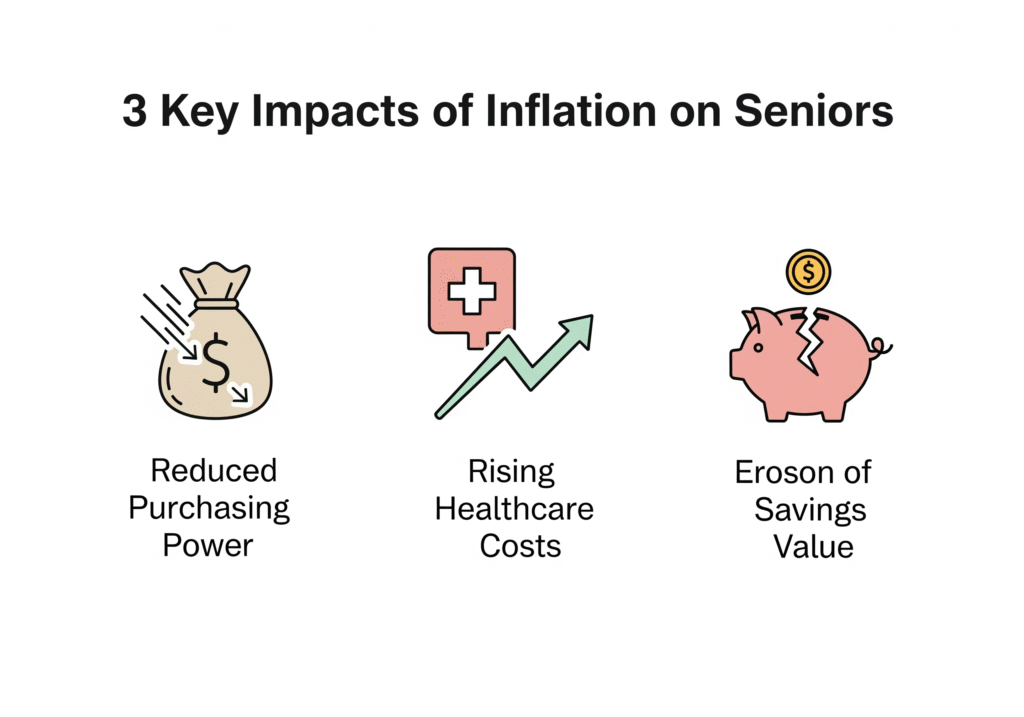

- Fixed Incomes: Many retirees rely on Social Security, pensions, and fixed annuities, which may not always keep pace with rapidly rising prices. Even Cost of Living Adjustments (COLAs) might lag behind actual inflation.

- Healthcare Costs: Healthcare expenses, including Medicare premiums, co-pays, and prescription drugs, often increase at a faster rate than general inflation, putting a significant strain on senior budgets.

- Savings Erosion: Inflation reduces the real value of savings held in low-interest accounts. What your money could buy a year ago, it buys less of today.

Therefore, proactive financial planning advice is paramount for seniors to safeguard their financial security.

💡 For an in-depth look at how inflation can affect your retirement savings, see the Report to Congress on the Impact of Inflation on Retirement Savings. U.S. Department of Labor.

Essential Financial Strategies to Combat Inflation

Here are actionable strategies that seniors can implement to navigate inflation effectively:

- Revisit Your Budget: The first step is to thoroughly review your current budget. Track your income and expenses diligently to identify areas where you might be able to cut back or make adjustments. Be realistic about rising costs in categories like groceries, utilities, and transportation. Look for non-essential spending that can be reduced or eliminated. Applying diligent budgeting tips is more critical than ever.

- Maximize Social Security and Pension Benefits: Ensure you are claiming your Social Security benefits at the optimal time for your situation. Understand how COLAs work and what to expect. If you have a pension, review its terms and any potential inflation adjustments. Exploring strategies to potentially maximize social security benefits (as discussed in a previous article) can provide a crucial income boost.

- Optimize Your Investment Portfolio (with Caution): While maintaining a conservative approach is generally wise in retirement, holding too much cash in low-interest accounts can lead to a significant erosion of its real value due to inflation. Consider diversifying a portion of your portfolio into assets that have the potential to outpace inflation over the long term, such as carefully chosen dividend-paying stocks or inflation-protected securities (TIPS). However, always consult with a qualified financial advisor before making any changes to your investment strategy, especially considering your risk tolerance and time horizon. This is a key aspect of sound fi planning.

- Explore Energy Efficiency and Cost-Saving Measures at Home: Implement strategies to reduce your utility bills. Consider energy-efficient appliances, LED lighting, better insulation, and adjusting your thermostat. Look for programs or rebates that can help offset the cost of these upgrades. Simple cost cutting tips around the house can add up to significant savings.

- Take Advantage of Senior Discounts and Benefits: Many businesses and organizations offer discounts to seniors on everything from groceries and medications to transportation and entertainment. Make it a habit to inquire about senior discounts wherever you go. Explore programs that can help with healthcare costs, such as Medicare Savings Programs or pharmaceutical assistance programs. This falls under the umbrella of money saving effectively.

- Consider Downsizing or Relocating (If Appropriate): Housing is often the largest expense in retirement. If your current home is becoming too expensive to maintain due to rising property taxes, insurance, and utility costs, consider whether downsizing to a smaller home or relocating to a more affordable area might be a viable option. This is a significant decision that requires careful thought and planning, especially considering the information available on affordable housing for seniors.

- Delay Major Purchases (If Possible): With inflation driving up the prices of goods, consider postponing non-essential major purchases if you can. Waiting might allow prices to stabilize or give you more time to save.

- Stay Informed and Seek Professional Advice: The economic landscape is constantly changing. Stay informed about inflation trends and forecasts from reliable sources. Don’t hesitate to seek advice from a trusted financial planning advice professional who can help you tailor a strategy to your specific circumstances and goals.

Maintaining Financial Resilience in an Inflationary Environment

Navigating inflation requires a proactive and adaptable mindset. By implementing these money saving strategies and staying informed, seniors can build greater financial resilience and protect their hard-earned savings from the eroding effects of rising prices. Remember that even small adjustments to your budget and spending habits can make a significant difference over time in managing your personal finance.

👉 Securing Your Financial Future Amidst Inflation

While inflation presents real challenges for seniors, it is not insurmountable. By understanding its impact and taking proactive steps to manage your finances, you can navigate these turbulent economic waters with greater confidence and security. Revisit your budget, explore savings opportunities, optimize your investments cautiously, and seek professional guidance when needed. Taking control of your financial planning is the most powerful tool you have to protect your secure financial future and enjoy a worry-free retirement, even with the persistent pressures of inflation and the rising cost of living.

Frequently Asked Questions (FAQ)

Q1: How often should seniors review their budget during periods of high inflation? A1: It’s advisable to review your budget more frequently during periods of high inflation, at least quarterly, or even monthly if you notice significant price increases in essential categories like groceries or energy.

Q2: Are there any specific government programs to help seniors with inflation? A2: Keep an eye out for potential expansions or new programs aimed at assisting seniors with rising costs. Stay informed through senior advocacy groups and government websites about any available relief measures.

Q3: What is the best way for seniors to protect their savings from inflation without taking on too much risk? A3: Consider a balanced approach that may include a mix of high-yield savings accounts, certificates of deposit (CDs), and potentially a small allocation to inflation-protected securities (TIPS), always keeping your risk tolerance and financial goals in mind and consulting with a financial advisor.

Q4: How can seniors reduce their healthcare costs during inflation? A4: Review your Medicare plan options annually to ensure you have the most cost-effective coverage for your needs. Explore prescription drug assistance programs and discuss generic alternatives with your doctor.

Read also: To deepen your control over expenses in uncertain times, check out our Ultimate Retirement Budget Planner for Seniors: Stretch Every Dollar.

Mantenha -se informado e procure aconselhamento profissional